Effective savings in 2026 use a combination of deposit accounts, not just one. A layered approach utilizes a regular savings account for short-term needs, a money market for higher balances, and a certificate of deposit (CD) to lock in stronger, fixed rates for defined timelines. This structure grows money efficiently while ensuring accessibility.

Despite Federal Reserve rate cuts in late 2025, competitive savings and CD yields can still outpace inflation. Locking in CD rates protects against further declines, while liquid savings offer flexibility. The best strategy matches these accounts to specific goals and timelines.

The right approach fits your timeline, goals, and commitment level. The strategies below are effective for all experience levels, from opening a first account to restructuring an existing portfolio.

Understanding Savings Accounts and CDs: How They Work and Why You Need Both in 2026

Achieving financial security requires combining multiple deposit accounts, each serving a specific role. A regular savings account provides immediate liquidity for short-term needs and emergencies and pays a modest, variable dividend rate. A certificate of deposit (CD) or share certificate, however, locks funds for a fixed term (e.g., three months to five years) in exchange for a higher, fixed dividend rate. Using them together creates a layered system: the savings account keeps emergency and short-term funds accessible, while the CD maximizes returns on money earmarked for future goals, such as a down payment or renovation. This strategy ensures every dollar is earning the appropriate return while remaining available when needed.

Both account types at federally insured credit unions are protected by the National Credit Union Share Insurance Fund, administered by the NCUA. According to the NCUA's share insurance documentation, member accounts are insured up to $250,000 per individual depositor, which functions equivalently to FDIC coverage at banks. This protection applies to share savings accounts, share certificates, money market accounts, and other qualifying deposits, providing the same federal backing regardless of which vehicle you choose.

If you have not yet established a checking account as the foundation of your banking relationship, our complete guide to checking accounts walks through how that piece fits with the savings strategy outlined here. A checking account funds your daily transactions, while savings accounts and CDs grow what you set aside.

Current CD Rates vs. Savings Account APYs: Where Your Money Grows Faster

The 2026 rate environment has reshaped how savers think about deposit accounts. After three Federal Reserve rate cuts in late 2025, the federal funds rate currently sits in a target range of 3-1/2 to 3-3/4 percent, the lowest level since 2022. Deposit rates have followed that movement downward, but competitive yields on both CDs and high-yield savings accounts can still outpace inflation, leaving real returns positive for savers who choose their accounts carefully.

What makes 2026 unusual is the relationship between short-term and long-term CD rates. Historically, longer commitments paid higher dividends to reward savers for tying up their money. The current market shows the opposite. The national average rate on a 12-month CD recently sat at 1.52%, while the average on a 60-month CD was lower at 1.34%. Short-term certificates currently outpace longer terms at many institutions, an inversion that reflects how rate expectations have shifted in recent cycles.

Savings account APYs fluctuate with market conditions, making them unpredictable for long-term planning but ideal for accessible funds. Unlike savings accounts, fixed-rate share certificates lock in a rate. Use a flexible savings or money market account for funds needed within six months. For money you can leave untouched for a year or more, a share certificate often earns more, especially when rates have recently fallen, protecting you from future rate drops.

National averages tell only part of the story. As a member-owned, not-for-profit cooperative, Florida Credit Union returns earnings to members through competitive dividend rates rather than passing them to outside shareholders. That structure, combined with NCUA share insurance protection up to $250,000, provides both competitive returns and federal backing on every qualifying deposit.

Comparing accurate rates means looking at the APY, not the nominal interest rate. APY (annual percentage yield) reflects the effect of compounding over a full year, giving you a true comparison between accounts that may compound monthly, quarterly, or daily. Two accounts advertising the same interest rate can produce different actual returns depending on how often dividends compound and post to your balance.

Building Your Emergency Fund: The 3-6 Month Rule and Where to Keep It

An emergency fund is the financial buffer that prevents an unexpected expense from becoming a long-term setback. The standard recommendation calls for three to six months of essential living expenses set aside in an accessible account. Three months suits households with stable employment, dual incomes, or strong professional networks that can shorten a job search. Six months makes more sense for single-income households, self-employed workers, or anyone in an industry with longer hiring cycles. The right target depends on how quickly you could replace your income if it stopped tomorrow.

Most Americans fall short of this benchmark. According to the Federal Reserve's 2025 Survey of Household Economics and Decisionmaking, 55% of adults said they had set aside enough money to cover three months of expenses in an emergency or "rainy day" fund. That leaves nearly half of households without a meaningful buffer against job loss, medical bills, or other significant disruptions. The same survey found that 37% of adults could not cover an unexpected $400 expense using cash or its equivalent, a figure that has held steady for several years.

To calculate your emergency fund target, focus on essential monthly expenses (housing, utilities, groceries, insurance, transportation, minimum debt payments, etc.), not total spending. Multiply this figure by three to six months. For instance, $3,500 in essential expenses requires $10,500 to $21,000. Accumulate this goal gradually.

Keep these funds in liquid accounts with competitive dividends, like a savings or money market account. These are federally insured and can be accessed quickly. Avoid certificates of deposit (CDs); the early withdrawal penalties and access constraints outweigh the slightly higher interest rate for emergency funds.

Building an emergency fund works best when you treat it as a non-negotiable monthly expense. Start with a target of $1,000 to handle minor emergencies, then build toward one full month of expenses, then continue adding until you reach your three-to-six-month target. Florida Credit Union's interactive financial education platform offers self-paced modules on budgeting, savings habits, and managing financial setbacks, which can support you during the longer climb to a fully funded reserve.

How much do most Americans have in emergency savings?

Just over half of U.S. adults have enough emergency savings to cover three months of expenses. The Federal Reserve's 2024 Survey of Household Economics and Decisionmaking found that 55% of adults reported having a rainy-day fund covering three months of expenses, up slightly from 54% in 2023 but still below the 2021 high of 59%. The survey also found that 30% of adults said they could not cover three months of expenses by any means, including borrowing or selling assets.

CD Laddering Strategy: Maximizing Returns While Maintaining Access to Your Money

CD laddering resolves the conflict of certificate investing by dividing funds across multiple CDs with staggered maturity dates. Instead of placing $10,000 into a single five-year CD, you split it into five $2,000 portions for one through five-year terms. When the one-year CD matures, you roll it into a new five-year CD. This system means one CD matures each year, providing regular access to funds, while the rest earns competitive, long-term rates.

The strategy offers three main benefits: yearly access prevents early withdrawal penalties; most funds earn the typically higher rates of longer-term CDs; and reinvestment risk is spread over multiple years. A shorter ladder, such as a 2-year plan with 6- to 24-month terms, also works for shorter time horizons.

Laddering is especially useful now. With short-term rates often higher, a ladder captures those rates today while gradually positioning longer-term funds for potential future rate increases. The strategy provides predictable rates without committing your entire balance to a single rate environment.

Building your first ladder does not require sophisticated tools. Most savers start with whatever amount they have available, divide it into three to five equal portions, and open certificates with staggered terms. Florida Credit Union offers share certificates with flexible terms from 6 months to 5 years, with a $1,000 minimum deposit, making laddering accessible for savers who want to start with smaller amounts and add to the ladder as their savings grow.

High-Yield Savings Accounts Explained: Online Banks vs. Traditional Banks

High-yield savings accounts have changed how Americans think about their idle cash. The "high-yield" designation simply means the account pays a dividend rate substantially above the national average for traditional savings accounts. The mechanism behind these higher rates is straightforward: institutions with lower overhead can pass those savings to depositors in the form of higher APYs.

Online-only banks built their entire business model around this advantage. Without physical branches, brick-and-mortar real estate costs, or large in-person staff requirements, they redirect those savings into competitive yields. The result is savings account APYs that can be several percentage points higher than those offered by traditional brick-and-mortar banks on standard savings products. The trade-off is that online banks generally cannot offer in-person service, cash deposit options at owned ATMs, or the relationship banking that comes with a local branch.

Traditional banks operate on a different premise. The expense of maintaining branches, ATM networks, and full-service teams shows up in the rates they pay on standard savings accounts, which often sit close to the national average. Many traditional banks now offer high-yield options to compete with online institutions, but those products sometimes carry higher minimum balance requirements, monthly maintenance fees that waive only with specific conditions, or rate tiers that drop sharply once your balance exceeds a certain threshold.

Member-owned credit unions occupy a useful middle ground in this comparison. At Florida Credit Union, members can deposit cash at a teller, speak with a representative about their account, and access digital banking tools through FCU Anywhere online and mobile banking. The combination delivers the rate advantages associated with online institutions and the service advantages of a traditional brick-and-mortar relationship.

Online-only savings accounts offer higher rates but lack physical branches, require digital service, and complicate cash deposits/transfers. Credit unions provide competitive rates plus in-person services for complex transactions. The best choice depends on your usage habits, not marketing.

Beyond the rate, evaluate practical features like minimum deposit, balance requirements, withdrawal limits, mobile app quality, and integration with your checking account. A slightly lower rate account that is easy to use for regular saving may be better than a high-rate account with high access friction.

Fixed-Rate CDs vs. Variable-Rate Savings: Which Protects You from Rate Changes

Choosing between a fixed-rate CD and a variable-rate savings account is about managing risk. Fixed-rate CDs lock in a dividend rate for the entire term, insulating you from economic changes. Variable-rate savings accounts offer a rate that can fluctuate based on market conditions and the institution's decision. The best choice depends on your interest rate outlook and time horizon.

Fixed-rate CDs protect you from falling rates. When you open a 24-month certificate at a 4.00% APY, that rate stays in place for two full years, even if the broader economy moves into a sustained low-rate environment. Savers who locked in long-term CDs in 2023 and 2024, when the federal funds rate sat at a target range of 5-1/4 to 5-1/2 percent, are still earning higher fixed yields today while newer certificates pay less. The protection works because your contract sets the rate at the moment of deposit, and the institution cannot adjust it downward during the term. The flip side is that you are also locked out of higher rates if the economy moves the other direction.

Variable-rate savings accounts protect you from rising rates. When market rates climb, your savings account dividend can climb with them, often within weeks. Savers who held variable-rate accounts during the 2022-2023 rate-hike cycle saw their yields rise substantially as institutions competed for deposits in a rising-rate environment. The risk runs in the other direction. When rates fall, your variable yield falls too, sometimes faster than you might expect. The same flexibility that lets your rate climb also lets it drop.

The 2026 environment favors fixed-rate strategies for funds you can leave alone. The federal funds rate has held in a target range of 3-1/2 to 3-3/4 percent through the early months of the year, following three consecutive cuts in late 2025. In a holding or declining rate environment, locking in today's CD rates protects against further declines, while variable-rate savings accounts may see their APYs move with the broader rate environment.

A blended savings approach works best. Keep emergency/short-term funds in a flexible variable-rate savings or money market account. Put longer-term funds in fixed-rate share certificates to lock in yields. This combination hedges against both rising and falling interest rates, meaning you don't have to predict the future. This decision isn't permanent; variable accounts allow flexibility, and fixed certificates mature, allowing you to reassess the rate environment and adjust your savings structure as needed.

The Complete Guide to CD Terms: Choosing Between 3-Month, 1-Year, and 5-Year Options

The right CD term matches the maturity date with when you need the money. Too short, and you sacrifice yield; too long, and you risk an early withdrawal penalty.

Short-term (one year or less) CDs offer high rates for funds needed soon (e.g., taxes, purchases). Current rates are competitive, but you face reinvestment risk if rates fall.

Mid-term (one to three years) CDs suit goals beyond the immediate future (e.g., a car, a renovation, a wedding). These often offer better terms than rolling short-term CDs, insulating you longer from falling rates.

Long-term (three to five years) CDs are for confident savers who want a strong, extended fixed rate. While shorter terms might currently pay more due to the inverted rate environment, a five-year CD protects you from significant rate declines.

Pay attention to the maturity date. You have a brief grace period to withdraw or roll over funds. Missing this window often results in an automatic renewal at the current, potentially less favorable, rate for the original term. Set a reminder.

Florida Credit Union offers share certificates with flexible terms from 6 months to 5 years, with a $1,000 minimum deposit, so you can match certificate terms to multiple savings goals at once. Pairing a 6-month certificate for near-term needs with a 24-month certificate for mid-range goals and a 4-year certificate for longer horizons creates a structure that serves different parts of your financial life simultaneously.

Early Withdrawal Penalties Decoded: What It Really Costs to Access Your CD Early

CDs offer higher fixed rates in exchange for keeping funds deposited until maturity. Early withdrawal incurs a penalty, which can reduce dividends and, in rare cases, principal. Understanding this penalty is crucial as it can erase yield advantages. Penalties vary but usually scale with the CD's original term, measured in days of dividends. Withdrawing early can disproportionately damage your return, as the penalty is typically subtracted from earned dividends.

For example, on a $10,000, 24-month CD at 4.00% APY with a 180-day penalty, withdrawing at six months ($200 earned) means the $200 penalty essentially negates all earnings. Withdrawing after one year ($400 earned) cuts the effective yield in half.

Some institutions impose harsher penalties, such as a percentage of principal or a high minimum floor, which can result in losing part of your original deposit. Always review the truth-in-savings disclosure for promotional CDs.

No-penalty CDs offer flexibility for a slightly lower rate, allowing penalty-free withdrawal after a short initial period. While they offer access, a traditional higher-rate CD with proper planning often yields better results.

The best defense against penalties is matching the CD term to your actual needs. Use savings or money market accounts for uncertain timelines. The penalty exists to deter early withdrawal, so planning to never need the money is the simplest way to avoid it.

How much does an early CD withdrawal actually cost?

The cost of breaking a CD early depends on the institution's specific penalty structure, but federal regulations set a minimum floor. Under the Federal Reserve's Regulation D, funds withdrawn from a time deposit within the first six days of deposit are subject to a minimum penalty of at least seven days' simple interest on the amount withdrawn, with no maximum cap set by federal law. Beyond that initial six-day period, individual institutions set their own penalty structures, which are disclosed in the account agreement before you commit funds. Always review the truth-in-savings disclosure for the exact penalty terms before opening any certificate.

Automated Savings Strategies: Setting Up Systems That Build Wealth on Autopilot

Effective savers rely on automated systems, not willpower. Automated savings strategies move money to a savings account, money market account, or CD on a recurring schedule, removing the decision-making process. Consistency builds substantial reserves with minimal effort.

A simple automated strategy is a recurring transfer from checking to savings, scheduled after payday. Set an affordable amount through online banking. This "pay yourself first" principle works by moving the money before you can allocate it elsewhere, forcing you to adapt spending to what remains.

Direct deposit is another reliable option. It removes the manual step of depositing checks and provides a consistent foundation. Once paychecks reliably arrive on a known date, you can time recurring savings transfers to run shortly after, automating the entire flow from earning to saving.

Goal-specific savings accounts add another layer of automation by isolating funds for particular purposes. Florida Credit Union offers Holiday Club and Vacation Club savings accounts that let you make recurring contributions throughout the year, with balances automatically transferred at scheduled times. The Holiday Club balance transfers to your regular savings on November 15 each year, just before holiday spending typically begins. The Vacation Club distributes half its balance in June and half in July, timed for summer travel. These structures take a savings goal that often gets neglected and turn it into a hands-off process that completes on schedule.

Automating contributions to certificates and money market accounts works the same way. After you build a base savings reserve, set up recurring transfers that push a portion of your monthly savings into higher-yielding accounts on a regular schedule. A monthly transfer from your savings account to a money market account, or a quarterly transfer that funds a new certificate as part of a CD ladder, keeps your money working at a higher rate without requiring you to actively manage the process every month.

The key to making automation work is removing the friction that causes savers to abandon their plans. Set transfers to run automatically on payday rather than asking yourself each month whether you can afford to save. Adjust the amounts when your income changes rather than when you remember. Review the system quarterly to make sure it still matches your goals, but resist the urge to pause or modify it during normal spending months. The strength of automation comes from its consistency, and consistency works best when you stop deciding whether to follow through.

Florida Credit Union members can arrange direct deposit and set up automatic transfers between accounts through FCU Anywhere. The technology to automate your savings already exists; the only step that requires your active participation is the decision to turn it on.

How effective are automated savings transfers?

Automated transfers consistently outperform manual saving for most people. According to the Consumer Financial Protection Bureau's research on savings app strategies, guaranteed saving rules like saving every payday are associated with roughly a 1.5 to 3.5 times larger increase in the maximum amount saved within a year compared to contingent rules that depend on user behavior. The mechanism is straightforward: money moved automatically before it can be spent stays saved, while money that requires an active decision to move often does not.

Money Market Accounts vs. Savings Accounts vs. CDs: Picking the Right Account for Each Goal

Choosing the right account for each savings goal is less about finding the highest rate and more about matching the account's structure to how you plan to use the money. Each of the three primary savings vehicles serves a distinct purpose, and savers who use all three for different goals consistently build reserves more efficiently than those who default to a single account for everything.

Regular savings accounts are designed for accessibility. Funds remain available within hours, dividends compound on whatever balance you maintain, and the account integrates seamlessly with your checking account for transfers in either direction. The dividend rate is typically modest, but the trade-off makes sense for money that needs to be reachable on short notice. Emergency funds, the early stages of any savings goal, and short-term reserves all belong in a regular savings account where flexibility outweighs yield optimization.

Money market accounts occupy a middle position between savings accounts and certificates. They typically pay higher dividend rates than regular savings accounts in exchange for higher minimum balance requirements. Florida Credit Union's money market accounts require a $2,500 minimum to earn interest, with tiered rates that pay higher returns on larger balances. This structure makes money market accounts well-suited for funds that exceed your immediate access needs but that you do not want to lock away entirely. A fully funded emergency reserve, savings for a down payment that is one to two years away, or a buffer above your day-to-day savings can all earn more in a money market account than in a regular savings account.

Certificates of deposit serve goals with defined timelines and money you have genuinely set aside. The fixed rate and term commitment work in your favor when you can match the maturity date to a specific need, such as a planned major purchase, a goal with a known target date, or funds that simply do not need to be accessible. The higher rate compensates you for the access constraint, and the constraint itself reinforces the savings discipline by removing the temptation to redirect the money before it serves its intended purpose.

A practical example shows how the three accounts work together. Suppose you have $25,000 in total savings allocated as follows: $10,000 in a regular savings account as your accessible emergency fund, $10,000 in a money market account earning a higher rate while remaining available for larger unexpected needs, and $5,000 in a 24-month share certificate locked in at a fixed rate as part of a longer-term goal. Each portion of your savings is positioned for the role it actually plays in your financial life. The emergency reserve stays liquid, the medium-term funds earn more than they would in basic savings, and the long-term portion captures a stronger fixed yield without sacrificing the accessibility of the funds you might need first.

Layering accounts this way also protects you against rate environment shifts. If rates rise, your variable-rate savings and money market accounts adjust upward over time. If rates fall, your fixed-rate certificate continues paying its locked-in yield. The structure builds in resilience without requiring you to predict which way rates will move next.

If you have not yet established the foundational checking account that supports this account structure, our complete guide to checking accounts covers how that piece fits with the savings strategy outlined here. Your checking account funds your day-to-day transactions, while your savings, money market, and certificate accounts grow what you set aside for different purposes and timelines.

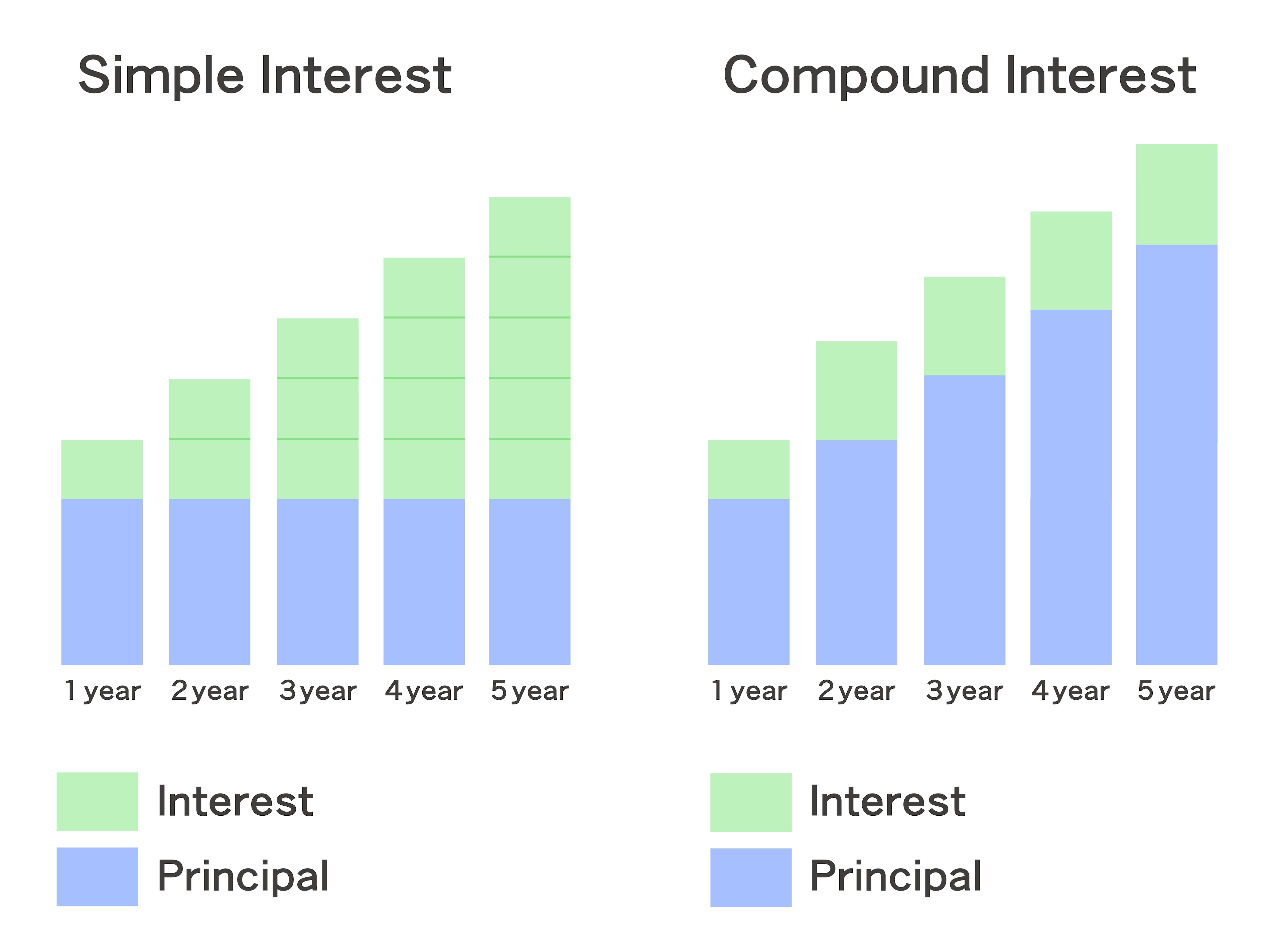

Compound Interest and APY Calculations: How Your Savings Actually Grow Over Time

Compound interest is the mechanism that turns consistent saving into meaningful wealth over time. The principle is simple: when your savings earn dividends, those dividends become part of your balance, and the next round of dividends is calculated on the larger total. Over months and years, the effect snowballs. Money you saved years ago is now generating dividends on top of the dividends it already earned, creating a growth curve that accelerates the longer your funds stay invested.

Simple interest, by contrast, pays dividends only on your original principal. A $10,000 deposit earning 4% simple interest pays $400 every year, indefinitely. The same $10,000 earning 4% compound interest pays $400 in year one, then earns 4% on $10,400 in year two, then 4% on $10,816 in year three, and so on. After ten years, the simple interest account has grown to $14,000. The compound interest account has grown to roughly $14,802. The difference looks modest in early years but widens substantially over longer time horizons.

APY, or annual percentage yield, is the figure that lets you compare accounts accurately by accounting for compounding frequency. Two accounts can advertise the same nominal interest rate, but if one compounds daily and the other compounds quarterly, the daily-compounding account will produce a higher actual return. APY captures this difference by expressing the total return you would earn over a full year, including the effect of how often dividends are credited to your balance. Always compare APY to APY when evaluating accounts, since interest rate alone can be misleading.

Florida Credit Union's certificates of deposit follow a daily compounding structure, with dividends compounded daily and credited to your account quarterly. This approach means your dividends start earning their own dividends within days of the original deposit, accelerating the compounding effect over the term of the certificate. The longer your money stays invested, the more pronounced the compounding benefit becomes, which is one of the structural advantages of certificates over accounts that compound less frequently.

The compounding advantage gets stronger as your time horizon extends. A 12-month certificate earns most of its value from the principal itself, since one year is not enough time for substantial compounding to occur. A five-year certificate, on the other hand, generates meaningful returns from the compounding of dividends earned in earlier years. Saving for goals that are several years away allows compound interest to do work that no amount of additional contribution can replicate. Time is the variable that makes compounding powerful, and time is the only input you cannot manufacture later.

This is also why starting earlier matters more than starting with a larger amount. A saver who deposits $5,000 at age 25 and lets it compound at 4% APY for 40 years ends up with a substantially larger balance than a saver who deposits $10,000 at age 50 and lets it compound for 15 years. The earlier saver contributed half as much money but allowed compounding to operate over more than twice the time. The lesson is straightforward: start with whatever you can save now, and let compounding contribute the work that you cannot do through additional savings alone.

How does compound interest actually grow your money?

Compound interest grows your savings by paying dividends on both your original principal and any dividends you have already earned, creating a growth curve that accelerates over time. The U.S. Securities and Exchange Commission defines compound interest as "interest paid on principal and on accumulated interest," which means each dividend payment becomes part of the base on which your next dividend is calculated on. The longer your money stays invested, the more pronounced the effect becomes, which is why time horizon is one of the most important variables in any savings strategy.

Common Savings Mistakes That Cost You Thousands in Lost Interest

Most savers lose money to small, repeatable mistakes rather than to dramatic financial setbacks. The cumulative effect of suboptimal decisions over the years often exceeds what any single emergency or market downturn would cost. Identifying these mistakes early and correcting them is one of the highest-leverage actions you can take to improve your financial position over time.

The most common mistake is leaving large balances in checking accounts that pay little or no dividends. A checking account is designed for transactions, not for storing money. Funds that sit in checking beyond what you need for monthly expenses are essentially earning nothing while inflation continues to reduce their purchasing power. Moving even a few thousand dollars from a low-yield checking account to a savings or money market account can produce meaningful annual gains without changing how you actually use the money.

Failing to use a CD ladder or any time-locked savings vehicle is another mistake that compounds over the years. Savers who keep all their funds in regular savings accounts capture the access advantage but leave significant yield on the table for money they could comfortably commit to a fixed-rate certificate. Even a single 12-month or 24-month share certificate for a portion of your reserves can meaningfully improve your overall return without seriously affecting your liquidity. The mistake is treating all savings as if they need to be immediately accessible when, in practice, only a portion ever does.

Breaking CDs early erases the rate advantage that motivated opening them in the first place. Savers sometimes commit to a 36-month or 60-month certificate for funds they ultimately need within a year, then pay an early withdrawal penalty that wipes out the dividend benefit and sometimes more. Before opening any certificate, pressure-test your timeline. If there is any meaningful chance you will need the funds before maturity, choose a shorter term or use a savings or money market account instead. The penalty cost of a single early withdrawal often exceeds the dividend gain from several years of correct CD selections.

Ignoring APY differences between accounts costs savers more than they realize. The difference between a 0.10% APY and a 4.00% APY on a $20,000 balance is roughly $780 per year. Over a decade, the gap exceeds $9,000 in dividend income alone, before accounting for the compounding effect of those earnings. Yet many savers leave funds in low-yield accounts simply because they have not compared APYs in years. Reviewing your accounts annually and moving funds to higher-yielding options when appropriate is one of the simplest ways to add meaningful returns to your savings.

Skipping automation is the mistake that affects savers across all skill levels. Even people who understand the importance of consistent saving struggle to follow through manually month after month. The friction of remembering, deciding, and executing each transfer is enough to derail even motivated savers during busy or financially tight months. Automated transfers remove the decision from your monthly routine, which is the only consistent way to ensure that saving actually happens. The savers who build the largest reserves are usually those who set up systems and let them run, not those with the strongest willpower.

Florida Credit Union's interactive financial education platform covers the foundational habits that prevent these mistakes from compounding over time, including budgeting frameworks, account selection guidance, and goal-setting strategies. Avoiding the most common errors is not about financial sophistication; it is about understanding which decisions matter most and building habits that handle them automatically.

Frequently Asked Questions About Savings Accounts and CDs

What is the difference between a savings account and a CD?

A savings account keeps your funds liquid and accessible at any time, paying a variable dividend rate that can change based on market conditions. A certificate of deposit, also called a share certificate at credit unions, locks your funds in for a fixed term in exchange for a higher fixed dividend rate. Savings accounts work well for emergency reserves and short-term goals where access matters most. CDs work well for funds you have set aside for a specific timeline and do not need to touch before maturity.

How much money should I keep in savings versus a CD?

Keep three to six months of essential expenses in a regular savings or money market account as your emergency reserve. Money beyond that amount, particularly funds earmarked for goals more than a year away, often earns more in a fixed-rate certificate. The right balance depends on your timeline and how much liquidity you actually need. Funds you might genuinely need on short notice belong in a savings account; funds you have already committed to a future purpose can typically work harder in a certificate.

Are credit union savings accounts and CDs federally insured?

Yes. Member accounts at federally insured credit unions are protected by the National Credit Union Share Insurance Fund, administered by the NCUA. Coverage extends up to $250,000 per individual depositor, which functions equivalently to FDIC coverage at banks. The protection applies to share savings accounts, share certificates, money market accounts, and other qualifying deposits.

What happens when my CD matures?

When a certificate reaches its maturity date, you typically have a brief grace period to decide whether to withdraw the funds, transfer them to another account, or roll them into a new certificate. If you take no action, most institutions automatically renew the certificate at the then-current rate for the same term you originally chose. Florida Credit Union sends a notice a few weeks before maturity, and if no response is received, the certificate automatically renews at the most comparable rate and term offered at that time. Setting a calendar reminder for any upcoming maturity dates ensures the decision stays in your hands.

Can I add money to a CD after I open it?

Generally no. Most certificates require a single initial deposit that remains in the account for the full term, with no additional contributions allowed during the term. If you want to add more money to a CD-style savings strategy, you have two options: open a second share certificate with the additional funds, which works particularly well as part of a CD laddering strategy, or use a money market account where you can continue making deposits while still earning a higher rate than a regular savings account.